Last-Minute Retirement Planning [Emergency 911 Portfolio]

Note: Post may contain affiliate links.

It's not too late to get your retirement planning on track

Retirement is on life support here in America with the average retiree living on less than $2,000 a month.

In this video, we’ll look at how to start investing late in life so you’re eating steak instead of ramen noodles in retirement. I’ll show you an example retirement portfolio to grow your dough but without taking too much risk.

We're building a huge community on YouTube to beat your debt, make more money and start making money work for you. Click over to join us on the channel and start creating the financial future you deserve!

Join the Let's Talk Money community on YouTube!

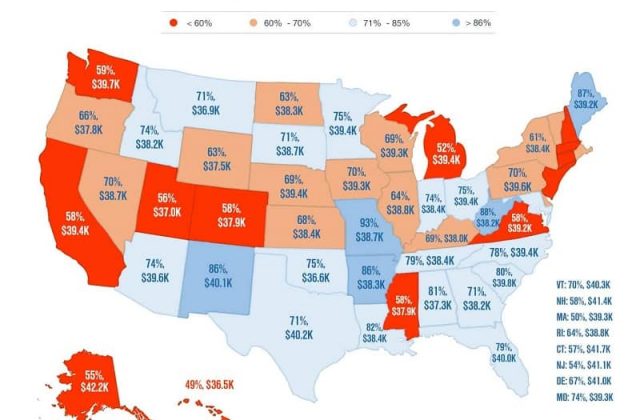

The Retirement Crisis in America

Nation, there is a retirement crisis in America so if you’re watching this video thinking you’re way behind…well, you’re not alone.

I took the average retirement savings by state, data from Personal Capital, and then used the 4% withdrawal rule for how much income those savings would produce. I took out state and federal capital gains taxes and finally added in social security benefits. So when we see here that the average Californian can expect about $39,000 a year in retirement; that’s based on about $28,000 in social security for a two-retiree household.

Needless to say, even if you’re able to count on two SSI checks a month, it’s just not enough to live on!

In fact, besides the average retirement income by state, you can also see how much that is as a percentage of the median household income. Using our Sunshine State resident again, that $39,000 annual retirement income is less than 60% of what most households live on. Put another way, our average Californian will need to cut $4 out of every $10 in their budget just to make ends meet.

Could you live on almost half your current expenses?

Of course, again, that’s assuming two social security checks AND the average savings.

And we know that a whole lot of people don’t have that average savings. More than four-in-ten Baby Boomers have less than $10,000 saved as they retire. More than three-in-ten of my own Gen X brothers and sisters have nothing saved and the average saved for all Gen Xers is under $30,000.

Nation, it is a hard life, retired on no savings. That’s where my mom found herself with less than $900 a month from social security. It’s subsidized housing and none of the bucket list you always expected of retirement.

A Last Minute Plan for Retirement Planning

We did a millennial investing video last week and I’ll do a video on investing during retirement next week but if you’re between 40 and 54 years old, I want you to come in real close to your phone, listen to what I’m going to say because this is going to be like an emergency 911 for your retirement!

I’ll show you how to start investing late in life, what NOT to do and an example portfolio for that last-minute retirement planning.

Now I want to start off with how to start saving more money and investing even if you haven’t been able to yet. Just five quick rules to saving that extra $100 a month.

That’s it, just focus on getting that $100 a month into your investing account because it might not seem like much but it’s really going to add up over time. Just $100 a month, even if you don’t get started until age 50, can create a $60,000 portfolio by the time you reach 70.

Is sixty-grand going to mean the high-life in retirement, maybe Miller High Life but it’s going to keep you out of the gutter and that’s what I want to do, get you to a point where you can still be happy in retirement.

5 Rules for Saving Money for Retirement

So rule number one here is you have to prioritize saving, take it off the top of your budget.

Tell me if this sounds familiar. You know how much you make each month, you list out all your bills and shocker, there’s nothing left over to save.

Now if you’re like most people, that’s not a bad situation, getting everything to come out even so there’s really no motivation to cut things from your budget. You’re making ends meet.

But those golden years are creeping up on you so unless you want them to be more like the copper years, we need to prioritize saving. And we’re going to do this by taking $100 off our income immediately, we’re going to have that money go directly into our investing account.

Then what happens? If you were just making ends meet, you’re going to come up short $100 on the bills, so you need to find somewhere to cut. It’s like a forced savings plan.

Next I want you to make sure you balance debt payoff and investing.

Debt free is all the rage and there are a lot of people out there that will say don’t invest a dime until you’ve paid off all your debt.

You know what I say?…Bullshit!

I’m not trying to be negative here but the tragic fact is that some people are addicted to spending. If they’ve got room in their credit card or cash in the bank, they’ll spend it and they may never be completely debt free.

But you know what we will all be someday, god willing, old and needing something to live on in retirement!

And all the debt-free fanatics, tell me in the comments how batshit crazy I am. I know it makes no sense on the numbers, investing $50 a month when you could get a guaranteed 12% return from paying down interest but I’m not being logical here, I’m being human.

Our behaviors don’t always make sense and I can’t fix your spending problem. What I can do is make sure you’re also building a nest egg while you’re working on that debt.

So keep paying down your debt but take that $50, maybe even $100 a month to start investing.

Third here is little Johnny is gonna need to pay his own college bills.

Saving for your kids’ college tuition is a noble goal but at this point, you need to prioritize your own well-being. I know student loans suck but you kids having to pay off their loans isn’t going to suck as much as you living on government cheese for the rest of your life.

One of the most often neglected here is having enough insurance.

You don’t need a million-dollar policy but having enough health and life insurance will save your ass!

According to Fidelity, a 65-year old retired couple can expect to pay about $285,000 in medical costs through retirement. Health insurance gets expensive as you get older but getting that little blue pill without insurance is even more expensive.

While you’re still earning and your family is depending on that income, you also need life insurance. My dad died at 42 and didn’t have a dime to his name but what he did have was enough insurance that the bills didn’t pile up after he was gone.

The basic rule here is around five- to ten-times your annual salary in life insurance. You might not need that much but you definitely need something while your family is depending on that paycheck.

Our fifth rule for saving and investing more before we get to what not to do is looking at the other side of the equation, making more money.

This is an investing video, I know, but you can’t invest what you don’t have and sometimes you just can’t budget and save any more money.

That means, you’re going to need to look at ways to make a little extra cash.

We’re not talking a part-time job here. We’ve got a lot of videos on the channel, side hustle ideas you can work as little as five or ten hours a week. That’s going to be just enough to get you that extra few hundred a month to invest.

Biggest Retirement Investing Mistakes

Before we get to that example portfolio for your last-minute retirement plan, I want to reveal the biggest mistakes investors make. This one will not only keep you from growing your money but will destroy everything you’ve built.

So you’ve started late but you figure if you can just make twenty- or thirty-percent a year, you’ll catch up in no time. So you look for the trading strategies, the penny stocks and you remember all the money people made in bitcoin a few years ago.

You cannot take these big risks with your money!

First of all, if it were so easy to make that twenty- or thirty-percent a year return, why isn’t everyone doing it? The fact is that anything over a 12% annual return is probably going to have a whole lot of risk that you’ll lose money instead.

And the tragic irony here is that you actually need to be taking less risk if you’ve started investing later or don’t have as much as you need. I know it sounds intuitive to go after those big risks, hoping for the bigger returns, but you’re turning your retirement plan into a trip to Vegas!

Yeah, that sixty-grand saved for retirement means you’re not visiting Paris, France. What happens when you lose that money thinking you’re going to be the next Wolf of Wall Street? Now you can’t even visit Paris, Texas!

So avoid the get-rich schemes and high-risk investing ideas. No penny stocks, bitcoin or futures trading, please.

Example Portfolios for Late Retirement Planning

But on to our example portfolio for late retirement planning and I just want to make a few suggestions on how to invest, what kinds of investments to hold.

First off, you’re probably going to want to rebalance your portfolio for how much you have in stocks, bonds and real estate.

If you’re like most investors, you’ve probably got a dangerously high amount in stocks…like everything. That’s fine for growth when the market is rising but what happens when stocks aren’t doing so well? At this point, you might not have time to let your portfolio recover from a stock market crash so you need the protection you’ll get in bonds and real estate.

How much you have in these could be wildly different between those of you in your early 40s and those getting closer to retirement. For us younger Gen Xers, we can still probably have close to 60% of our money in stocks, maybe 15% in bonds and 25% in real estate.

In your 50s and approaching 60s though, you’re going to want to shift that gradually to something like 50% in stocks, twenty- or twenty-five percent in bonds and 25% or 30% in real estate.

Just like we talked about earlier with taking less risk if you’re way off your retirement goals, that’s going to affect how much you want in stocks as you get closer to retirement. If you’re sitting at less than one-hundred grand in savings, maybe you want even more in bonds and real estate funds for that cash flow you’re going to need to live on and the safety from a stock crash.

Some kind of direct real estate like a rental can be a great investment at this point. The kids are becoming more independent so maybe you’ve got a little more free time. You’re probably making more so can really use the depreciation and other tax shields you get from real estate.

Within the stock portion of your portfolio, focusing on dividend stocks can be a good strategy to start building that cash flow and get a sense for how much just that income source can be in retirement.

Now when you’re picking dividend stocks, remember you still need a balanced portfolio so don’t go picking only REITs or BDCs or shares of utility companies. Look for some good dividend payers in tech and consumer discretionary for that growth component as well.

Here I’ve used a few ETFs to show what a simple portfolio might look like. This would be for younger Gen Xers in their 40s and we’ll look at another portfolio for older investors next. So you see we’ve got about 60% in three stock funds with a focus on dividends in those first two and even our growth fund pays a little cash flow.

I’ve got a long-term bond fund and even a little higher return with these high-yield bonds and then my favorite real estate fund, the VNQ, for our property exposure.

If you wanted to invest in a handful of individual stocks, maybe take 20% of your money out of the stock funds and invest across ten or fifteen stocks. This will give you that balanced return from the funds with safety in the three asset classes and then a chance for an extra return in the individual stocks.

The older investor’s portfolio is only slightly different with 50% in the stock funds and 25% in the two bond funds. I’ve still kept a little in that high-yield bond fund for some growth but we’ve got more safety in the long-term bond fund.

How you split this up or use different funds is up to you. The important point is having some money in each asset; stocks, bonds and real estate so you get that diversification and cash flow.

I know this might be a little disappointing to those that want a get-rich fast strategy; growing that $10,000 into a million kind of idea…but I don’t want you to lose what you have. There is still time to build that nest egg but not if you’re constantly making an omelet and having to start from scratch.

Leave a Reply

You must be logged in to post a comment.