How to Protect Your Money from a Stock Market Crash

Note: Post may contain affiliate links.

Learn how to protect your investments from a stock market crash with these tips from the experts

One of the most important lessons I’ve learned in more than a decade as an investment analyst is that you can’t time the next stock market crash.

You can follow the economic trends, adjusting a portion of your portfolio with business cycle investing. You can even rebalance your portfolio every few years to sell what’s gone up and buy assets that have lagged.

But trying to jump in and out of stocks before a crash isn’t going to end well.

Even the large banks and venture capital firms I’ve worked for were extremely hesitant to make short-term timing decisions.

Nobody knows when stocks will tumble. The only certainty is that they will eventually. So even as 2022 looks like the year the stock market crashes, especially after stocks have already fallen about 10% on average since the beginning of the year, anyone saying they KNOW how the rest of the year will play out is trying to sell you a load of bull.

While you can’t time the market, there are things you can do to protect your investments when the bottom does drop out. There are stocks that do better during a market crash and even investments that will not only protect your portfolio but grow it!

I reached out to 10 investing experts for their favorite ways to protect against the next stock market crash.

FREE WEBINAR – Discover how to create a personal investing plan and beat your goals in less than an hour. Step-by-step to the Goals-Based Investing Strategy I developed while working in private wealth management.

Reserve Your Spot on the Next Webinar Now!

Checklist for Protecting Your Retirement Savings from a Stock Market Crash

A lot of what we heard came back to five keys to protecting your investments when the markets fall.

- Holding more than just stocks and bonds in your portfolio. Other assets like real estate, peer to peer loans and crowdfunding investments will help smooth out your returns.

- Rebalancing not only helps to protect your money but will also keep you on track for your retirement goals.

- Understanding your risk tolerance and how much changes in the stock market cause you stress will help guide your investments.

- Your investments should change as you age to better match your goals and risk tolerance.

- Have investing rules like when to sell so you don’t freak out and make snap decisions like panic selling.

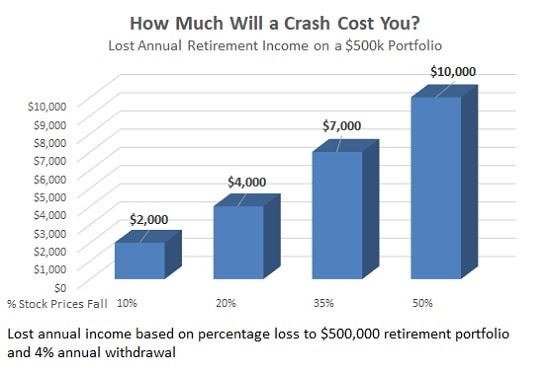

How Much Would a Stock Market Crash Hit Your Retirement Savings?

Investors talk about a stock market crash but corrections where stock prices fall more than 10% are far more likely and can cause just as much pain. A correction is when stocks fall at least 10% from the prior peak while a stock crash is when the market is down 20% or more.

The 19 corrections over the last 50 years have wiped out about 14% on average. It’s taken about 200 days for the stock market to rebound from one of these corrections.

While stocks have always recovered from these hiccups, memory of those big crashes always puts investors on edge. As prices fall into that 10% range from their highs, investors start to worry if it isn’t the start of a much bigger drop.

For those getting ready to retire a correction is painful but not the end of the world. A 14% drop on a $500,000 portfolio wipes out $70,000 and reduces retirement income by just under $3,000 a year.

The problem is when investors scramble to protect their money after a correction has already begun. They start selling stocks at the worst moment, locking in those losses and never giving their investments time to recover. Even worse is that investors then wait too long to start buying stocks again, waiting until prices have already rebounded from a market selloff.

FREE Report! See the 5 Biggest Stock Positions in My Portfolio! Five stocks I'm investing in for the biggest trends of the next decade! Don't Miss this Free Report – Click Here!

General Strategies for Protecting Your Investments

The last 50 years has seen seven periods where stocks fell more than 20% from their peak, with the last two in 2000 and 2008 being the worst of the group. Seven crashes in 50 years doesn’t sound so bad but there’s also been 19 corrections where the S&P 500 fell more than 10% from its peak level.

Keeping your cool when stocks sink may be a matter of keeping a long-term focus and doing what you can to protect your investments ahead of time.

The most frequent advice I heard from the group of experts was to worry less about a stock crash and just invest in a general strategy that meets your needs. This means putting together an investor policy statement (IPS) and understanding your own tolerance for investing risk.

Rob at Dough Roller warned against making short-term decisions for the dire mistakes they usually cause.

We cannot predict future stock market returns, period. Warren Buffett himself says he can't predict future market returns. Why should we fool ourselves into believing we can out smart Buffett?

That doesn't mean, however, that there's nothing we can do to prepare for financial downturns. Rob suggests these four steps to prepare your investments for any investing environment:

- Set our allocation between stocks and bonds at level that we can accept in a down market. Start at 70/30 as a baseline, and then decide if you can handle more volatility.

- Keep your debt low. Handling a bear market is about a lot more than our investments. We need to take a holistic approach to our finances. Keep debt levels down will help us weather a stock market crash.

- Don't invest money in the market that you will need to spend in the next five years.

- Invest primary in index funds. They are inexpensive and outperform most actively managed funds. As importantly, when they are down, we don't have to worry about whether the money manager has lost his or her touch.

Dian at EconMatters offered a few more general tips for investing in good times and in bad:

- Review your portfolio and be willing to take gains (and even losses) off the table. Cash in king.

- Keep cash in FDIC insured accounts. Know the FDIC limit and spread your cash accounts if necessary.

- Pay off all debt (mortgage, car, TV, etc.) and try to build one-year living expenses in liquid Rainy Day Fund.

Investing in Real Assets to Balance Financial Asset Risk

As a financial asset, stocks and bonds depend on the value of the company they represent. Without the company or its future outlook, those stocks and bonds are worth only the value of the paper itself…nothing.

Balance your financial assets with investments in real assets like real estate. Real property has actual physical demand that gives it value even when the market tumbles. That helps to support your wealth and real estate provides a great tax shelter on earnings.

For most investors, direct ownership of real estate isn't the best way to go. It costs hundreds of thousands to buy a few properties and you still may not be diversified across property types or regions. Besides the problem of diversification, property management can be a full-time job.

A better way to get access to this asset may be in the new crowdfunding opportunity.

Instead of having to manage your own properties, something that can be a full-time job itself, you can invest in multiple projects alongside professional developers.

Real estate developers and other investors offer their projects on real estate crowdfunding sites. The platforms have analysts that verify the properties and the developer's history with only about 5% of submitted deals making it in front of investors. Investors can then pick which deals in which they want to invest, usually as little as $1,000 per investment.

Besides the opportunity for professional management of your investments, crowdfunding allows you to diversify your portfolio with deals in different property types and across the country for a fraction of the cost it would take with direct ownership.

I follow several real estate platforms but invest most of my money on Fundrise. It costs nothing extra to have an account on more than one crowdfunding site and you’ll be able to invest in more deals.

The Only Guaranteed Positive Return in a Stock Market Crash

Want to know the one investment to provide a guaranteed positive return even during a stock market crash?

Dividend stocks!

While the price of dividend-paying stocks may sink with the rest of the market, that cash payment you receive will always be a gain.

Here’s what the Dividend Growth Investor had to say about protecting his portfolio with dividend stocks.

I am a buy and hold investor, who invests money to work every single month. I try to build a diversified portfolio of dividend growth stocks by focusing on companies that have raised dividends for at least 10 years in a row.

I find it easier to focus on the dividend stream that my portfolio generates, than to focus on share prices which are dictated by short-termism and human emotions such as fear and/or greed. Dividends from a diversified portfolio of US stocks have been very stable and growing over time.

I know that during the next bear market, my portfolio will keep generating dividends to pay expenses. I don’t really have to worry about stock price fluctuations. The best way to ensure that I won’t do anything stupid is by focusing on the dividend income stream and ignoring the stock market.

Having a diversified portfolio helps immensely – this should include representation from as many sectors as possible and having at least 40 – 60 individual securities.

The stock market has bounced back after every prior crash and will again after the next one. If you don’t panic and sell during the next bear market, and if you don’t panic and try to time the market during a bull market, but stick to your plan, you should be fine.

Enjoying that positive cash return doesn’t just have to come from dividend stocks. Check out MLPs, REITs and fixed-income investments for consistent cash flow and less risk compared to stocks.

Protecting Your Money with Other Assets

Investors are terribly under-invested in other assets like bonds and real estate. I get it, stocks are the sexy investment and offer the potential for huge returns.

But it’s in these other assets that you’ll find some of the best protection when stock prices plunge. Bonds and real estate react differently to the economy and will help support your portfolio with consistent cash flow.

Derek of Life and My Finances recommends real estate rentals for cash flow and diversification.

So many people blindly put money into their 401k and assume it will grow into something they can retire on. This is an extremely bad plan for one main reason, lack of diversification. Sure, they might have money in three or four different funds, but it's still fully invested in stocks and is entirely dependent on market growth. In the event of a crash, they're absolutely screwed.

To combat this, my wife and I invest roughly half of our nest egg into real estate for which we pay cash. Not only do the rentals provide us an income, but the property appreciates in value year after year as well! Even if the stock market takes another dive, chances are that real estate won't go along with it.

Rob at Passion Saving suggests investors rebalance their portfolio regularly.

To avoid losing too much in a market crash, investors should lower their stock allocations when prices get insanely high (like they are today!). It's not a good idea to get out of stocks entirely because it is not possible say precisely when a crash will come. But it makes all the sense in the world to lower one's stock allocation a bit because all lasting crashes take place starting from high prices.

That allocation Rob talks about is the percentage of your total wealth you have in the different assets. Everyone has a target of how much they need in stocks, bonds and real estate to balance out rough times but provide enough return to meet their goals.

Part of putting together your investor policy statement and finding that perfect target allocation is understanding how your investments change with your age.

Are Bonds Safe in a Stock Market Crash?

Bonds used to be the ‘safety’ investments that investors could count on when stocks tumbled. That’s been the rule over the last 30 years because interest rates have been on a long, downward trend.

Since bond prices increase when interest rates fall, bonds have always provided this upside protection.

That might not be the case over the next 30 years.

The rate on the 10-year Treasury bond hit a rock bottom of 1.37% in 2016 and rates on government debt in other countries was negative. The 10-year rate has climbed to 2.76% after five rate hikes by the Federal Reserve and at least two more are on the way this year.

Bonds will still pay semi-annual interest but as interest rates increase, the value of those bonds you hold will fall. That might not be enough to take the return to zero and surely bonds won’t destroy value like stocks do in a crash, but they won’t be the safety asset any longer.

That’s why it is more important than ever to invest in other assets beyond stocks and bonds. Neither of these assets is going to give you the return and protection you could count on in years past.

I’ve invested most of my portfolio in real estate and p2p lending to make up for the problems in stocks and bonds.

- Peer loans give me the return of stocks but are still fixed-income investments, so they aren’t as risky.

- Real estate crowdfunding gives me a direct ownership in property and cash flows but without the hassle of managing my own rentals.

Seeking Safety in a Stock Market Selloff

When stocks do crumble, you’ll hear a lot about safety assets and a flight to quality. This happens when investors take shelter in a crisis, selling anything risky and buying the safest investment that will protect their money even if it means little or no return.

In the past, the flight to quality has been to hard assets like gold or those backed by the U.S. government like Treasury Bonds or even reserve currencies like the U.S. dollar or the Japanese Yen.

Steve Kanaval of Equities.com shared why he thinks digital currencies could be the next safety investment.

As a former portfolio manager, I have seen many hedges for your portfolio. From buying puts to selling calls and using a myriad of ETFs, the choices in the hedging world are limitless. Now with Bitcoin we need to see if this proves to be a flight to quality in the times of panic. The best example would be to look at the events around Brexit last year. We saw a major flight to quality, and many managers chose to grab some downside protection.

The only one that paid off was Bitcoin.

The best way to hedge your portfolio strictly in equities is to pick a small number of stocks and own them for the long haul. When they have sharp sell offs, buy more and put them away.

Solid advice, but investors should broaden their horizons to encompass digital currency, as the fallacy of global fiat currency is insane in the social media world we live in today. Trust in the government is eroding, as is the reporting needed to only use a dollar denominated unit of measure in a world where block chain and liquid, easy to use Bitcoins are in your digital wallet and you can buy anything from an airline ticket to a car on auction on eBay.

Full adoption is around the corner, and it’s conceivable that cash in our society will become obsolete in our lifetime. Protecting your portfolio from a market on a 10-year run will take creative thinking on the part of investors who have been trained to take the easy road by investing in mutual funds, ETFs and listening to brokers who sell product with the highest commissions. The best idea for investors who have profits in stocks is to start looking at digital currency and work to understand the current flight to quality trends in the markets today.

Taking a Long-Term Focus to Ride Out Roller-Coaster Stock Prices

One of my favorite ways to invest is on themes. These are long-term trends around factors like the aging population, the energy revolution or the emergence of China as a superpower.

These trends run for multiple decades and are driven by forces larger than a single business cycle. Investing in companies that benefit from these big picture trends means your portfolio will bounce back quick even if the market crashes.

Not only is theme investing a great long-term strategy but it's a perfect fit for 401k investing because the time horizons match up so well.

Vintage Value Investing offered its favorite long-term investing theme, one I’ve been watching for a few years as well.

One of the best investments for the next 10 years will be… water! According to the U.N., water usage has grown twice as fast as the world's population over the last century. Today, we use about 30% of the world's total accessible renewal supply of water. In less than 10 years, that percentage could reach 70%.

By 2025, almost 2 billion people will live in areas plagued by water scarcity, with 75% of the world's population living in water-stressed regions!

Billy at Retire Early Lifestyle suggests to use index ETFs such as the Vanguard Total Market Index as a core holding.

A rough guide is to subtract your age from 120 in order to see what percentage of your investable assets should be placed in equities.

How to Protect 401K from a Stock Market Crash

One of the things I like about investing in a 401K plan, besides the free money from a company match, is that investors are less likely to stress out during a stock market crash.

401K investments are usually in broad-based funds spread across hundreds of stocks so they tend to follow the market instead of troubles in one particular stock. This can still be stressful when the entire stock market falls but it’s usually a smoother ride.

Protecting your 401K from a stock market crash is a combination of taking the long-term view, rebalancing every few years and slowly changing your investments as you age.

- If you have more than 10 years to retirement, you may not have to do anything. The stock market typically recovers its prior high within five to ten years even after a crash.

- Understand how much of your money you want in stocks and bonds depending on your age and risk tolerance. This will help protect your money as you get closer to retirement.

It’s also smart to rebalance your 401K investments every few years to keep on your target for stocks and bonds. A few years into a bull market, consider transferring some of the funds in your stocks to a bond fund to protect the money. After the stock market has fallen 10% or 20%, consider moving some of the money from bonds back into stocks.

Do You Need to Worry about a Stock Market Crash?

There were two experts that said don’t worry about the next market crash. I like to rebalance, selling some stocks after a few years of market gains and refilling my allocation in bonds, but generally don’t worry much about a stock market crash either.

Evan of My Journey to Millions took the conversation back to the bigger picture with your investing goals and, “I honestly do not think you can protect against a stock market crash, and that's okay! Make sure your risk tolerance matches your asset allocation and ride it out knowing that you should have time to let it all work itself out. It is unlikely that the next crash is going to be the one that destroys our market system.”

FIDough backed this up with, “Lots of research shows that most people tend to sell near the bottom, and reenter the market after it has gone up significantly. In other words, most people do worse by trying to protect their money from market crashes. The truth is, if you keep on investing and stick to your rebalancing plan throughout market cycles, you will do great.”

Always keep your focus on your long-term investing goals and avoid making those short-term decisions trying to time the market. Follow some of the ideas above to protect your investments but don’t try to get out of stocks the day before the next selloff. When the next crash comes, stay calm and keep investing!

Don’t Miss the Stock Market Crash Series and Protect Your Money!

- How to Invest Before a Stock Market Crash

- Ultimate Guide How to Invest Money for Beginners

- How Many Shares of Stock to Make $1000 a Month?

Leave a Reply

You must be logged in to post a comment.