3 Ways to Fix Real Estate Investing

Note: Post may contain affiliate links.

Real Estate Investing is Broken but I've got How to Fix it!

I bet you didn’t know real estate investing was broken, did you? Then why is the default rate on investment properties 65% higher than on owner-occupied?

In this video, I’m detailing the three biggest risks in real estate investments and how to fix all three.

We’re building a huge community of people ready to beat debt, make more money and make their money work for them. Subscribe and join the community to create the financial future you deserve. It’s free and you’ll never miss a video.

Join the Let’s Talk Money community on YouTube!

How to Get Started Real Estate Investing

We love real estate investing here in the nation. No other asset has created as much family wealth as property and I truly believe all investors should have real estate in their portfolio.

BUT… there are a lot of pitfalls in property investing that you just don’t see starting out. You get roped into rentals or some other strategy after hearing some get rich scheme and it’s only after putting down tens of thousands do you realize those common mistakes.

I’ve been there. I left a job as a commercial property analyst in 2003 to start in residential real estate. The housing boom was just picking up and that’s where the money was being made.

Then I made all the mistakes we’ll talk about in this video. Three mistakes that bankrupt tens of thousands of real estate investors every year. In fact, research by the Housing Finance Policy Center on residential investment properties found the default rate of loans by investors was 29% higher than owner-occupied loans.

What are the Biggest Mistakes New Real Estate Investors Make?

These biggest three risks in real estate investing go beyond the problem of property as a passive income investment. We covered that last week in another video and I shared three ways to make your real estate strategy as passive as possible.

No these three mistakes are ones almost every beginner real estate investor makes and you might not even realize they’re leading you to bankruptcy…not until it’s too late.

So let’s look at the three problems, then I’m going to show you how to fix them all with one investment.

Fundrise is a new type of real estate investing, a portfolio of cash-flow properties managed by professionals for stress-free investing. The platform is offering new investors a 90-day risk-free trial. Try it out and if you're not totally satisfied, you get your entire investment refunded!

Learn more and try Fundrise for 90-days risk-free!

Too Much Real Estate Debt

The first problem new investors get into is putting on too much debt when they buy property.

That same study found the average debt-to-income for investors was 35% and a loan-to-value average of 80% for investment properties. Worse was that more than a third, 35% of the properties had loans above 80% of the property value.

This was a huge influence in the fact that investors were 29% more likely to default on their property loans. Not only are investors over-extended on their investment properties but they’re also likely to be over-leveraged on their own home mortgage as well, making any hiccup in cash flow a one-way ticket to bankruptcy.

Now when we talk about how to fix these problems, I’ll show you how to estimate cash flow on a property so you know exactly how much debt you can afford.

Investing in the Wrong Property Type

Another big mistake beginner real estate investors make is the property type they buy and I’m not talking about buying residential or commercial property, I’m talking about only buying that one property type.

It’s estimated that just over 11% of the U.S. adult population invests in real estate or about 26 million people. Of that, more than 18 million investors own only residential rental houses. Almost seven-in-ten investors are completely invested in just one property type.

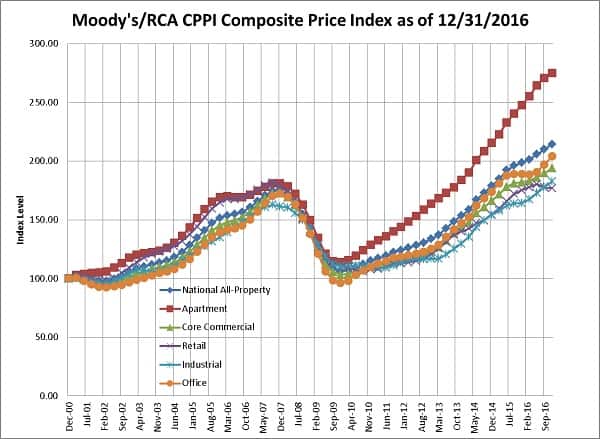

That’s a huge problem when something happens to decrease prices in that property type. This graphic is a bit jumbled but it shows the index level prices for five property types; apartments, core commercial, retail, industrial, office and then the all-property level from 2000 through 2016.

And if you follow that red line for apartments, that property type was one of the most volatile after the housing bubble burst. Even though home prices have rebounded faster than other property types, it was a rough ride there for a while. Instead if you were investing in a mix of property types, you would have seen a much smoother ride with lower vacancy and more stable cash flows.

Investing in the Wrong Location

The third mistake here before we get to how to fix these is the region or location investors buy and again, we’re talking about only buying into one region.

Now this one is more easily understood. Most real estate investors manage their own properties so it obviously makes sense to have them grouped in the local market.

Again though, that opens investors up to a huge amount of risk when that market is hit harder than others. Data from Standard & Poor’s here shows the housing price change in select cities after the crash. With a nationwide average of 33% loss, some of these markets were absolutely destroyed.

Phoenix saw prices crash 54%, San Diego and LA were both down 40%. New York saw prices fall only 24% but then only saw an 8% rebound against a nationwide average of 28% from 2012 through 2014.

How to Fix Beginner Real Estate Problems

Now I want to show you how to fix these problems, how to invest in real estate without the three most common mistakes. First though, I want to get your experience. What problems have you seen in real estate investing? Which are the most common and how did you solve them? Just scroll down and tell us in the comments below.

First I’m going to tackle that problem of debt and defaults by showing you how to calculate your cash flow on a property. We’ll look at how to estimate expenses before you take out the loan to make sure you have a cash cushion to save your ass when you need it.

I’ll then show you how to fix the other two problems with a single investment, how to get those property types and a portfolio of investments in different regions with one investment.

How to Estimate Real Estate Cash Flow

And on estimating those cash flows, you really have to write it all out. I know there are all kinds of rules like estimating 50% of the rent to go to expenses but they do absolutely nothing for you. It’s so general that it can’t possibly tell you anything useful about your investment.

So take the time here and work through these numbers because this will save you a ton of heartache.

Here I’ve put together some estimates from experience and we’ll talk about how to find the actual numbers for properties in your area. Basically you’re working down from how much rent you can collect through all your expenses to see what kind of cash flow a property produces after paying the mortgage. You need to be building up a cash cushion from that money so if something goes wrong, you can keep up with the mortgage without going broke.

You should know about how much you can get for a property in rent. If not, look at similar properties in the area. For vacancies, I usually estimated about one month a year or 8% of the rent lost. This is going to depend on whether you’re in a nice neighborhood with low vacancy rates or investin’ in the hood where you might have two or three tenants come and go inside a year.

Next you’re going to estimate all the expenses to keep the property up. Again, you want to find the exact amount you can expect but I’ve included estimates as well.

For utilities, even if you have tenants pay these, you’re going to be on the hook for when the place is vacant and when tenants just run out and don’t pay the bill so I’d estimate at least 10% of your rent.

Repairs and maintenance will differ depending on age of the property and your region as well as if you’re including appliances. A good rule is between 10% to 15% but you might want to estimate on the high side if you don’t know. Remember, you might not spend this every year but then a big expense like the roof or HVAC might come up and be thousands of dollars.

Property management is generally 10% of the rent but that’s if it’s even available in your market. Smaller cities might not have good managers available or they’ll cost more. You can save this amount but you better be ready to handle calls at 2am and a constant headache.

Property taxes range from just a quarter of a percent in Hawaii to as high as 2.4% of the home’s value in New Jersey. The average is around 1.2% but check with your local assessor. These are usually paid twice a year so don’t forget to plan for it.

I used to estimate around 2% for tenant marketing and again, that’s an average off every month so you have that cash reserve when tenants leave and you have to find new ones.

Insurance is going to vary depending on the types you need but don’t get cheap here. I had a boss that let his homeowner’s policy lapse because he was selling the house and thought it would sell fast. Fire ripped through and he was out tens of thousands of dollars in a heartbeat.

Mortgage insurance is around a percent of the loan amount if you’re loan-to-value is 80% or above. That can easily be a couple grand and is just another reason to not borrow too much on your property.

Homeowners’ and flood insurance will run you from half a percent to a full percent of the home’s value if you need them both. The nationwide average for home insurance is just over $1,000 a year but that ranges as low as $590 in Delaware to over $2,000 a year for the average home in Florida.

Legal and permitting is the last expense we’ll estimate and this is going to include things like evicting tenants and getting a rental certificate.

Now on these estimates, and PLEASE find the numbers specific to your target investment if you can, but on these numbers you’d have 50% of your monthly rent left over. This is why that 50% rule is so common because it’s pretty close to reality but pretty close doesn’t cut it when the difference is between profits and bankruptcy.

After taking all these numbers out, then your mortgage payment, you’ve got an estimate of cash flow left over each month. I would say, for safety’s sake, you want this to be at least 20% to 25% of your rent.

How to Start a Real Estate Portfolio

So that helps fix the problem of debt and defaults for investors but what about the other two problems, only investing in one property type or in one region? These two can have a huge effect on your ability to pay the mortgage because when something drives up vacancies for that single property type or in your local market, your estimates could be thrown out the window.

The problem here is that most investors just don’t have the bankroll to buy a diversified portfolio. You’d need at least 12 properties to diversify into three property types in each of the four regions of the U.S. and even that’s going to be highly risky on each property. For a truly diversified portfolio, I would say you need closer to 24 properties or more.

For this, there is no better solution than investing part of your portfolio in funds of real estate investment trusts or on Fundrise.

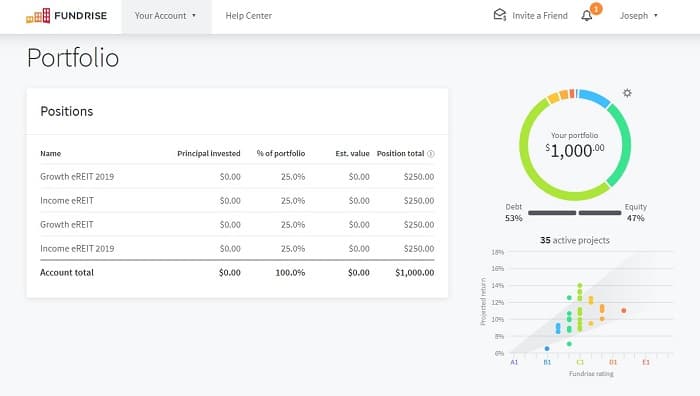

We’ve talked about REITs on the channel before but I just got started last month on Fundrise. I’ve got over $26,000 in REITs in an IRA account, ten grand in other property funds and another $300,000 in rental property equity. I took a thousand from the REIT portfolio and invested on Fundrise for a little higher return.

With that portfolio investment on Fundrise, I get exposure to 35 properties in different markets and across property types. Returns on the platform have ranged from 8.5% to over 12% since 2014 and cash flow is as high as 8% in the Supplemental Income portfolio.

So if you’ve got that direct real estate exposure to a specific property type or in a single market, for example local rental properties, you can take maybe ten- to twenty-percent and invest in broad, diversified real estate funds. That’s going to shift your risk away from the single property type or market.

What I like about Fundrise and why I finally signed up is the complete transparency on all the investments. You can see how each property stacks up on risk as well as how many are debt investments and how many are equity.

You can click through to see individual properties like this commercial renovation in California. The platform is going to show you the project risk, what type of investment the portfolio has as well as a full market analysis.

And again, that diversification of property types is important here. You’ve got commercial properties like the office space we just looked at and residential space like this apartment project. You’ve got those debt investments that provide safety and income as well as the equity projects that help boost returns for the portfolios.

One feature that really sets Fundrise apart is this 90-day trial offer and low $500 minimum. Invest as little as $500 in the starter portfolio and try it out for 90-days. If you’re not totally satisfied, you get your entire investment returned.

Learn more and try Fundrise for 90-days risk-free!

Don't avoid these three real estate investing mistakes. It will cost you unimaginable headaches and tens of thousands of dollars…minimum. Know how to invest in real estate and avoid the biggest problems for beginner investors.

Leave a Reply

You must be logged in to post a comment.