5 Catastrophic Risks in 401k Loans

Note: Post may contain affiliate links.

401k loans may seem like a good idea but the facts prove they are traps waiting to happen

When you’re in a pinch and need money, it can be tempting to consider taking a loan from your 401k plan. After all, the money is yours and when you pay it back, you’re paying yourself back.

You wouldn’t be alone. Some 11% of workers took 401k loans during the past year, with an average loan amount of $9,500 borrowed from their retirement account.

But although it may seem harmless, taking a loan from your 401k can have negative consequences, especially for the 40% of borrowers who decrease their savings rate after taking a loan.

Research shows that taking money from your workplace retirement plan, even when you intend to pay it back, can have a lasting impact on your future retirement savings.

Here are five reasons to think twice before taking a 401k loan from your retirement plan:

1. Many don’t continue to save at the same rate on their 401k after taking out a loan.

Taking a loan may affect how much you can afford to contribute to your retirement plan. Paying back what you borrowed may leave you with less money to contribute.

In a Fidelity study of 401k loans taken from 2007 to 2013, almost one-in-four of the borrowers decreased their savings rate in the first year after a loan was taken. One-in-ten people stopped making contributions altogether.

In a Fidelity study of 401k loans taken from 2007 to 2013, almost one-in-four of the borrowers decreased their savings rate in the first year after a loan was taken. One-in-ten people stopped making contributions altogether.

And the numbers get worse over time. Borrowers further along in their repayments were more likely to have decreased their contributions.

In fact, within five years, 40% of borrowers had reduced their savings rate from pre-loan levels and 15% had stopped saving altogether.

The effects of reducing or stopping your 401k contributions are catastrophic to your retirement savings. For example, consider two employees, age 25, who each earn $50,000 and defer 10% annually in a traditional 401k.

The first employee takes a 401k loan and maintains his contributions until retirement and beyond. At retirement, his 401k balance is $537,000 or about $2,237 in monthly income.

The second employee also takes a 401k loan, but instead of keeping up his contribution rate, he reduces his investments to nothing for 10 years and then resumes his original savings rate. His plan balance at retirement is $396,000—producing an estimated monthly income of $1,960, or $690 less per month than the employee who kept up with his contributions.

2. A 401k loan diminishes the tax advantages of saving in a 401k.

You contribute pretax dollars to a traditional workplace retirement account. You don’t pay income taxes on the contributions or their growth until you begin taking withdrawals during retirement (unless you take early withdrawals, which are subject to both income tax and a potential 10% IRS penalty).

The combination of those tax advantages and the potential of your investment portfolio to grow give your savings the boost you may need in retirement.

When you take a loan from a traditional 401k, you may have a negative impact on the tax deferral benefits. Here’s how:

- You lose any tax-deferred growth the borrowed funds would have generated in the plan.

- You repay your 401k loan with after-tax dollars. And then you’ll have to pay taxes on those funds again, when you withdraw them at retirement.

- Your pretax plan contributions lower your tax bill; if you reduce them, you may face higher taxes for the year.

3. If you’re borrowing to buy a home, the impact may be greater.

Borrowers taking home loans from their 401ks represent just under 3% of people with 401k loans, but the number has been increasing steadily since 2009.

These loans can have an outsized impact on your financial future because people tend to borrow more on 401k home loans. The average 401k home loan is $23,500 for more than two-and-a-half times larger than the average 401k loan.

That’s problematic for a few reasons:

- 401k home loan borrowers typically pay back the debt over periods of 10 years. That’s a long time to miss out on the growth of the loan amount.

- For some people, it’s hard to get back on track to saving for retirement—not to mention paying off student loans, credit card balances, and other debts—so they wind up reducing their retirement contributions.

- Many investors who take out home loans aren’t saving enough to begin with. Here's an easy guide on how much to save and retirement X-Factors that affect the size of your nest egg.

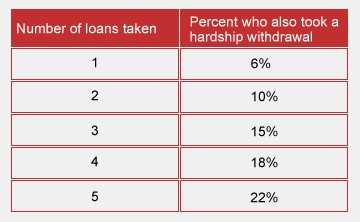

4. 401k loans can lead to serial borrowing.

Your first 401k loan can be like a gateway loan that leads to habitual borrowing from your retirement account. Fidelity analysis of 401k investors shows that one out of two 401k borrowers went on to take additional loans.

In some of these cases, outside circumstances lead the investor to take each one of these loans, so it isn’t always the case that one loan is the direct cause of the one that follows it; but all too often it seems that the first loan makes it easier to take a second, the second led to a third, and so on.

There is also a correlation between loans and hardship withdrawals: The more loans a participant takes, the more apt he or she is to take a hardship withdrawal as well (although once again, it isn’t always the case that loans are the direct cause of hardship withdrawals).

Hardship withdrawals are withdrawals permitted by your plan for specific expenses, which can range from medical expenses to college tuition. Unlike plan loans, hardship withdrawals cannot be repaid. The money is taken permanently out of your account, which could have long-term ramifications on your financial security in retirement.

After you take a hardship withdrawal, you are generally prohibited from making contributions to your plan for six months, must pay income tax on the amount you withdraw, and may be subject to 10% penalty if you are under age 59½, for taking an early distribution, and you might be subject to a state penalty as well.

Consider opening a Roth IRA for your retirement savings. While it's still not a good idea, you can always withdraw your Roth contributions without a penalty or tax.

5. You’ll have to repay the loan quickly if you leave your job for any reason.

You typically have to repay any outstanding balance on your 401k loan within 60 days when you separate from the company that offers the retirement plan. Employees usually stay at their jobs for about four-and-a-half years, according to a 2014 survey from the Bureau of Labor Statistics.

If you plan to take a loan from your retirement plan, you’ll want to consider how long you plan to remain at your job, and whether that timeline fits with the duration of the loan. Be especially wary of borrowing from your plan if you think you could be laid off or fired.

Taking a loan from your 401k is a big decision, and not to be taken lightly. In a 2011 Fidelity survey, nearly 40% of retirees who had taken a loan said that they would not do so again, and a third of plan participants who had not yet retired agreed with that sentiment.

Ask yourself these questions before taking your 401k loan and potentially setting yourself back in retirement.

- Do you have a plan for how to repay the loan?

- Have you calculated how much the loan will affect your retirement savings?

- Do you have a repayment plan if you leave your job?

- Will borrowing the money solve your financial problem or will you just need to borrow more in the future?

Before you tap into your retirement savings with a 401k loan, be sure to look carefully at your finances. These retirement account loans can seem like the easy solution but they’re filled with all kinds of hidden traps and worries. They can seriously set your retirement planning back and should only be used as a last resort.

Leave a Reply

You must be logged in to post a comment.